Thomas Weisman • November 12, 2021Perspectives

Why every company should care about fintech

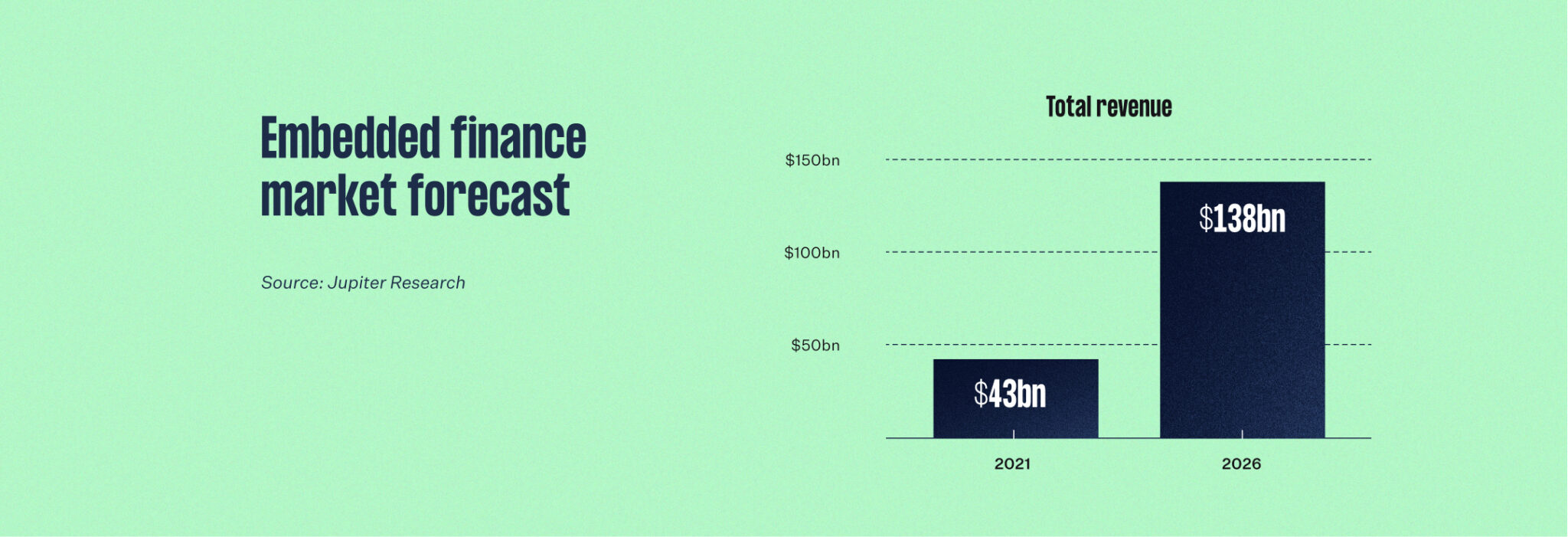

Embedded finance is allowing scores of businesses to expand into financial services—and grow their TAM along the way

- Fintech has emerged as a new tech platform that empowers businesses to offer payments and other financial products as a service

- Embedding fintech services allows businesses to deepen their relationships with customers and gather data to serve them better

- As with cloud, mobile or the internet itself, early adopters of embedded finance will gain an edge over rivals

Shopify, the e-commerce powerhouse, began its life in 2006 as a subscription service for merchants to design, set up and manage their online stores. But early on, the company realized its merchants would benefit from an easy and seamlessly integrated way to get paid for the goods they sold. By 2013, Shopify introduced payments into the platform.

Over time, the data Shopify gathered on its customers’ transactions positioned it to start layering additional financial services to serve merchants, including credit-card processing, “buy-now-pay-later” options, lending and banking. Today, revenue from payments dwarfs the revenue Shopify gets from subscriptions. And the rapid growth of these financial services is largely responsible for the company’s $184 billion market valuation.

The rapid success of Shopify illustrates one of the most powerful market opportunities in tech: embedded finance.

Innovation fuels surge in embedded finance

Shopify may be among the first—and most successful—companies to embrace embedded finance. But in recent years, a growing number have jumped on the bandwagon.

Uber and Lyft have long offered an array of financial services that include instant payments, vehicle financing, debit cards and more to their drivers. Toast, which makes software for restaurants, has embedded financial products like loans, cards or insurance, in addition to payments, into its offerings, surfing the embedded finance wave to a $32 billion valuation. TurboTax maker Intuit has done the same for its small-business customers. The list goes on.

This democratization of financial services capabilities has been fueled by a wave of innovation in the fintech sector. A range of companies—from Affirm and Bill.com to Finix, Klarna, Plaid, Stripe and others—have empowered customers to access financial products through simple APIs. Together, they’ve created something of a new platform that can provision financial services on demand, much like AWS provisions cloud services on demand.

We believe it’s still early days for embedded finance. And opportunities abound for both fintech companies and the vertical platforms that adopt their services.

Opportunities for fintech: Powering a trend to exponential growth

For the fintech sector, creating products that can easily be embedded by their customers has been an undeniable boon. It has offered a simple mechanism for growing revenue exponentially without the need for large sales forces. A partnership with a software platform that has a large existing customer base instantly increases reach and revenue through long-term contracts.

The approach has minted scores of fintech unicorns and created opportunities for niche players. Take a company like Xplor Technologies, which offers business management SaaS and a cloud-based payment processing platform for businesses in “everyday life” verticals. The company, which is majority owned by Advent International, has quickly established itself as a powerhouse in the “subscription economy,” helping gyms, childcare centers and other small businesses manage their members and customers with payments and banking services embedded in its core SaaS offerings. It offers a clear playbook for new entrants in still-untapped customer segments.

Opportunities for SaaS platforms: Expanding TAM with sticky services

Embedded finance has been equally rewarding for those who have embraced it as customers. By integrating products like payments and lending, SaaS platforms get valuable data on the health of their customers, which they can leverage to improve their own offerings while managing risk. Financial services also create more sticky relationships which, over time, can greatly boost the value businesses derive from each customer and grow their total addressable market.

Indeed, analysis by the venture capital firm Andreessen Horowitz suggests vertical SaaS platforms that successfully add financial services to their offerings may see between a doubling and quintupling in revenue from existing customers. Over time, embedded financial services could become the majority of revenue for some platforms, as the Shopify example shows. They could even help to subsidize core SaaS offerings in industries that are particularly price-sensitive. For example, Silo, a platform for managing the supply chain for wholesale fresh produce, does this for a customer base reluctant to spend on software, but with a willing habit of paying for financial services.

By integrating products like payments and lending, SaaS platforms get valuable data on the health of their customers, which they can leverage to improve their own offerings while managing risk.

The potential scope of embedded finance is so large that the question is often how to get started. Integrations can be quite costly, so companies that want to bring fintech onto their platforms should think about rolling it out in stages. Payments are an obvious place to start. Many major corporations have not digitized their payment processes, even as consumers are expecting ease of use and flexibility for making payments digitally and through a range of vendors.

There’s no question that learning to leverage embedded finance will become a key strategic asset for scores of companies in the digital world. Just like with earlier technology platforms—cloud, mobile or the internet itself—early adoption could prove to be a key factor that separates winners and losers. Consumers and business customers are increasingly expecting to have simple, intuitive and powerful financial tools at their disposal, and companies that fail to meet those expectations risk losing out on the significant expansion and growth opportunities ahead.